Back when I was in banking, I always looked forward to certain annual vendor meetings and reports. These key partners provided valuable insight into what was happening beyond the four walls of our institution. Their input was essential to helping us assess our market position and refine our strategy.

Some of the most impactful reports were from BAI benchmarking, CSAT scores, Visa and Greenwich Associates. These sources tapped into our internal data and compared it with data from our industry peers – insights we couldn’t have accessed otherwise.

That’s why I’m excited about Intelligent banking: The future ahead, a new piece of primary research from The Economist Impact and SAS.

Based on a survey of more than 1,700 senior banking executives worldwide, plus comprehensive research and in-depth interviews, our new report identifies the most pressing trends and challenges facing the financial services industry over the next decade and explores how those priorities are shaping its future.

A follow-up to Banking in 2035: Three possible futures, a popular report we released three years ago, our new report builds on that foundation with fresh data, diverse executive perspectives and even more real-world insights. This blog post recaps key highlights from the latest report.

The AI-fraud arms race

While there were some outliers and surprises, the study’s results reveal a broad alignment across the industry. Banks recognize the shifts demanding their attention and are responding by strengthening foundational frameworks, evolving infrastructure, adopting and innovating with new technologies, upskilling talent and harnessing the agility of strong vendor and partner ecosystems.

Generative AI (GenAI) is emerging as both a threat and a tool in the ongoing battle against fraud. As scammers increasingly exploit deepfakes and synthetic identities, 54% of banking executives cite the growing complexity of fraud as their top concern. AI-powered detection holds significant promise, but high upfront costs and integration challenges continue to hinder adoption. Cloud-based AI services and embedding AI during product design are seen as more cost-effective alternatives.

Crucially, fraud detection models rely on unified, high-quality data – something many banks still lack. Data fragmentation across silos remains a persistent issue. To address this, institutions need stronger AI literacy among leadership and “AI evangelists” within business units to align teams on shared goals, capabilities and implementation strategies.

Data governance: From compliance to competitive advantage

AI’s effectiveness is inherently tied to data quality and security. As a result, data governance is becoming a cornerstone of technology transformation in banking. One-third of executives rank governance frameworks –policies governing data access, quality and compliance – as the most effective tool for ensuring data security, ahead of automation and AI-driven threat detection.

Some banks are taking proactive steps, such as DBS Bank’s PURE framework (Purposeful, Unsurprising, Respectful, Explainable), to guide ethical data use. The governance agenda is also expanding to include ownership models, traceability and preparation for disruptive technologies like quantum computing. Notably, retail banks – with their vast troves of consumer data – express greater concern about data quality than their corporate counterparts.

Regulation: Burden or catalyst?

While some governments are pushing to loosen legacy regulations, the regulatory landscape for AI, privacy and data sovereignty is becoming increasingly fragmented. The EU’s AI Act classifies AI-based financial decisioning as “high risk,” while US regulation remains piecemeal at the state level. Most banking leaders surveyed say they are less concerned about overregulation and more focused on the need for clarity and harmonization.

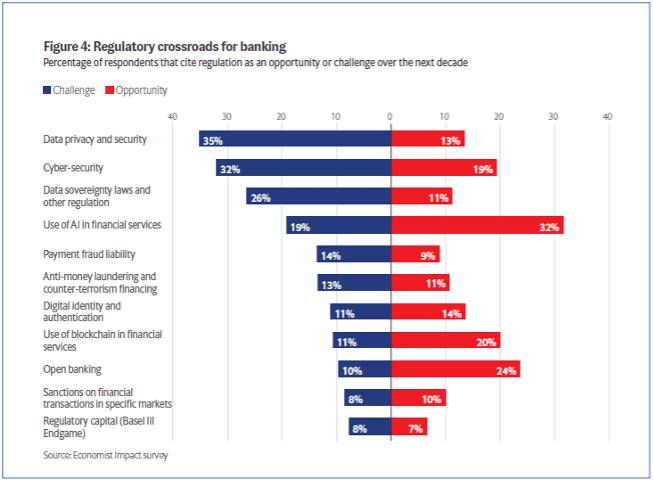

Despite rising compliance costs – reported by more than 75% of respondents – two-thirds of executives believe those costs are justified, given the reputational and legal risks of non-compliance. Looking ahead, three key areas of regulatory friction over the next decade include data privacy, cybersecurity, and data sovereignty (see Regulatory crossroads for banking, an excerpt from the report, below).

To manage growing complexity, banks are increasingly investing in compliance automation while also fostering deeper cross-functional collaboration between technical and compliance teams. Institutions like Aspire have restructured internal teams to better align these historically siloed functions.

Competitive disruption: From fintechs to CBDCs

Traditional banks are facing an existential threat on multiple fronts: Fintechs, digital-only banks, big tech and now central bank digital currencies (CBDCs). While fintechs continue to expand in payments and credit markets, big tech’s entry through mobile wallets and embedded finance signals deeper disruption.

At the same time, CBDCs pose a unique risk by potentially disintermediating banks by enabling consumers to hold deposits directly with central banks. Although many view CBDCs as a long-term threat, their potential to erode deposit bases, limit lending capacity and disrupt international payment flows should not be underestimated. As a result, strategic planning around digital assets – including custodial services and crypto risk management – is becoming a growing priority.

Innovation models: Build, buy or partner?

To remain relevant, banks must embrace continuous innovation – not just through technology adoption but through cultural transformation. While M&A activity continues, most executives view internal innovation and employee upskilling as more effective strategies. Acquisitions often fall short due to integration challenges and cultural misalignment.

Partnerships are increasingly seen as the most effective model for driving innovation. Collaborating with fintechs and big tech enables banks to scale offerings, reach new customer segments and access emerging technologies without heavy upfront investment.

However, these partnerships can also introduce new risks. Data-sharing with third parties is a top security concern, and inconsistencies in cybersecurity and compliance practices can expose banks to fraud and regulatory breaches. Joint governance committees and frameworks like the Financial Data Exchange (FDX) can help institutions maintain oversight and accountability within these complex ecosystems.

Priorities for banking leaders

To navigate the volatility ahead, banks must align risk, technology and innovation strategies around five imperatives. I won’t reveal them all here – you can see the complete list and expert insights in the full report.

Instead, I’ll share two strategies that are close to my heart as a former industry insider.

First, it’s critically important that banks strengthen data governance and AI governance. This includes building robust frameworks with clear ethical oversight, accountability and model auditability. “Having a strong governance framework is not optional,” says Zechariah Akinpelu, chief information security officer at Unity Bank.

It’s also necessary for financial institutions to earn customer trust. Long a hallmark of traditional banking, trust now requires a broader commitment. From transparency in AI-driven decisions to protecting sensitive data and continuously striving to improve the customer experience, banks must show they’re acting in customers’ best interests at every touchpoint.

As technologies mature and the regulatory perimeter evolves, banks must move beyond incremental change. Success in this new era requires risk leaders who can help reshape operating models, anticipate threats and turn compliance and governance into competitive advantages.

But don’t just take my word for it. There’s much more data, details and commentary from industry experts in Intelligent banking: The future ahead. The complete report also includes case studies from Standard Chartered, DBS, Revolut, Klarna and JPMorgan.

I hope this new primary research inspires fresh thinking or validates the strategies you’re already shaping at your institution just as similar insights once did for me.